|

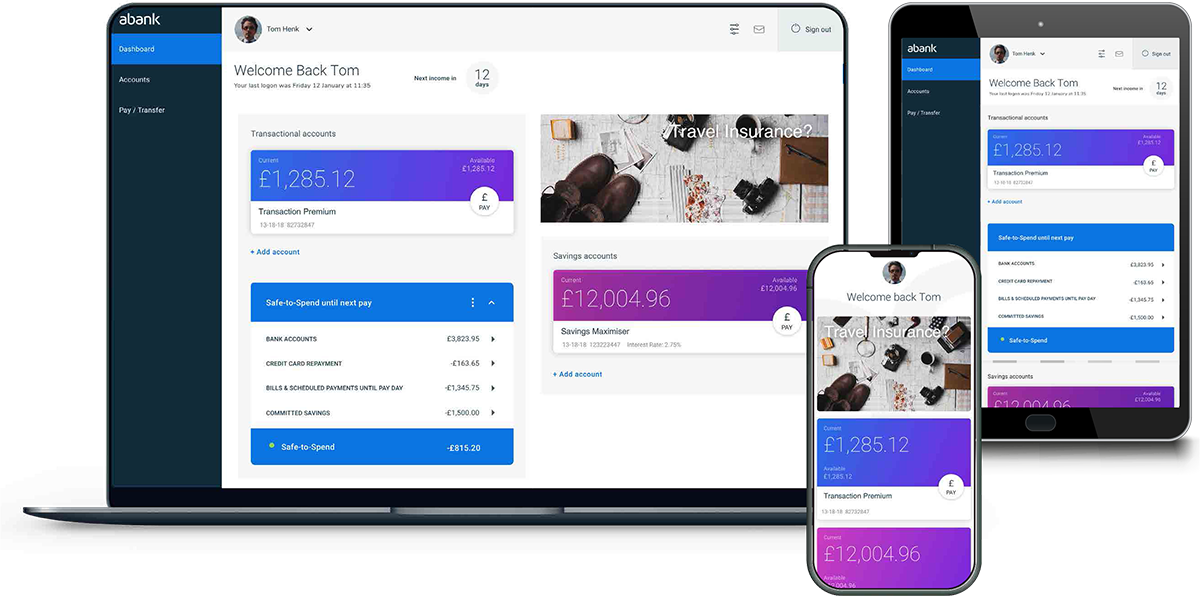

Mobile Financial Applications - The good, the poor as well as the hideous Mobile banking applications have actually commonly been deemed a price centre. Yet this undervalues their potential to be both a sales channel, and also a cost-reduction channel. They can play a key duty in the digitisation of several financial processes in a electronic improvement program. So what separates the excellent mobile banking apps from the negative? Sandstone Modern technology's Abhish Saha, Executive General Manager, Digital Banking and also Ranjan Kumar, Supervisor of Product Management, Digital Financial, share what they deem the qualities of good, poor ( as well as ugly) applications. The 7 indicators of a great mobile banking app 1. It's simple to make use of across all transaction as well as task kinds. As Kumar points out, this is a lot more crucial since the pandemic and also wider smart device fostering has opened up electronic banking technology up to a much wider market. 2. It offers immediate accessibility to functionality as well as experiences-- within a number of faucets. This should be a continuous focus for app programmers, Saha says. The app does not ask the client to touch or type greater than is definitely required. Keeping in mind typical tasks such as expense repayments and also account transfers is standard hygiene. 3. It's a single point of entry with one password, thumb print or face recognition to gain access to as numerous verified financial solutions as feasible to really equip the consumer to bank where as well as whenever they wish to, states Saha. It also satisfies customer expectations for capability, enabling consumers to transact, change preferences and communicate with the bank notices. 4. A excellent app enables a financial institution to communicate immediately with its customers in an authenticated fashion at a affordable, according to Saha. It provides a area for dedicated communications whether through conversation or messaging. It plays a major duty in ending the "unfriendly" phone call centre experiences that frustrate customers prior to they even reach review their discomfort factors, i.e., being asked multiple authentication concerns and also to recite pin numbers created years back. 5. On the financial institution side, a good mobile app should help with information as well as analytics, says Kumar. It should offer insights to the financial institution, which not just assist personalise product offers and also experiences, capitalizing on revenue possibilities, but likewise quickly determine the friction points for consumers. This can aid boost the general consumer experience. 6. Saha claims it's critical that the App lowers the financial institutions' Price to Income proportion, by eliminating non-revenue producing tasks from financial institution team in get in touch with centres, branches and procedures. That might mean offering consumers the capacity to turn their credit card on and off, set parameters around whether they will approve international payments, caution the financial institution that they're travelling and even manage conflicts and also restore Term Deposits. These drive excellent business situations for a financial institution by eliminating web traffic from higher cost networks such as contact centres and also branches. This also minimizes waiting time imposts on consumers. 7. A great financial application permits a bank to make deals, in addition to aid develop and enhance products based upon exactly how they resonate in market. Enabling customers to set up a term down payment reinvestment directions, foreign exchange trading or purchase an insurance plan on the move. shutterstock_1431992843 The 4 indicators of a negative mobile banking app 1. A negative mobile financial app stands alone. Ten years ago you might get away with an application resting off sideways because mobile apps were fairly new, Saha says. However today every application requires a alternative omni-channel strategy. It requires to enter into the remainder of the customer experience, linked to various other channels including branch networks as well as call centres. If something goes wrong in the app, a client needs to have the ability to call the bank's contact centre or walk right into a branch to complete the experience. If your application doesn't collaborate with the rest of the financial ecological community things can obtain unsightly. Customers anticipate continuity of service. 2. A poor app does not cover all market devices ¹ as well as browsers, so it will not deal with more recent models, or it only collaborates with more recent models. This problem is commonly ignored, particularly when developers are collaborating with minimal sources, are unskilled, or could just be evaluating on their own phones; so when they most likely to market, with the myriad of devices out there, the end individuals have a entire series of different experiences. It's only then that the bugs are identified. mobile phone banking trends

3. Core features are inefficient or tough to utilize in a bad mobile app. We recommend banks determine the 10 most typical tasks that a retail user or service user performs on the app and also concentrate on making those mobile use situations super-efficient. If they aren't easy, customers will discover a much better experience elsewhere-- even if they presently do all their banking with you. 4. Negative mobile banking apps crash or run slowly due to excessive bloatware. This typically happens when a financial institution is utilizing the application as a advertising channel, expecting customers to await promotions to load. Imagine the experience for a client who is delayed by doing this when attempting to make an vital payment promptly. In our experience, poor apps are usually the result of inexperience. Excellent apps are created by groups who have actually been through the same workout with other financial institutions and discovered the lessons.

0 Comments

Whether it is personalised content on your social networks feeds, advising Alexa to change the song or making use of FaceID to gain access to encrypted details on your cellular phone, Artificial Intelligence (AI) is something we can no more disregard and sometimes, we can't think of living without it. In this short article, we will certainly explore just how technical advancements and electronic transformation is motivating an AI-enabled future in monetary services. It is difficult to go over the duty of AI in monetary services without highlighting that 2020 was hugely disrupted by COVID-19 and the ripple effect is anticipated to last for several years. Financial Institutions electronic change strategies formerly specified for 2020 rapidly deciphered, exposing the inefficiencies to respond and also react rapidly when the pandemic grasped the globe at an unmatched rate. The reality is AI is experienced by most individuals from early morning until evening. There has actually been debate over the true meaning of AI as the assumptions on whaAI Robot-1t is deemed as 'real knowledge' modification so typically. At a high-level, AI as a field can be referred to as any type of method that enables machines to address a task like exactly how human beings would. Maybe leveraging Artificial intelligence, which utilises formulas to enable computers to pick up from instances without needing to be explicitly configured to choose; or All-natural Language Handling, which is concentrated on generating significance and intent from message in a legible, natural type, or Computer Vision, which is concentrated on extracting meaning as well as intent from visual aspects including pictures and also video clips. Accelerated digital improvement The increase of fintech and brand-new modern technologies over the last years has actually been considerable and also this has actually influenced just how clients engage with organisations and also in turn has changed the economic services landscape. Altering client expectations, strong competition, raising governing pressures and also the pressure to boost functional efficiency has actually seen the industry pressure itself into a reactive process where rate to market became even more important for survival. A brand-new age of open banking has allowed systems to swiftly and also seamlessly integrate with brand-new platforms and also applications. Physical banks and paper systems are swiftly being dated and also replaced by durable digital ecological communities, evident by the increasing introduction of brand-new digital only challenger financial institutions. Digital makeover simply put is to rethink what we currently produce based on new technologies available. It is the procedure of modernising what we have done prior to. A digital improvement method need to tailor an organisation's response to crises, altering consumer practices, and more comprehensive market conditions. It is right here that AI can really be leveraged.

AI quality in financial solutions Financial organisations are investing substantial amounts of capital in digital capacities such as chatbots, expert system (AI) and open APIs. The main breakthroughs over the past sixty years have been advancements in search formulas, artificial intelligence algorithms, as well as integrating analytical evaluation into comprehending the globe at big. The favorable influences that AI is having on financial solutions is expanding. Making use of AI in credit history decision-making has become progressively widespread, with the potential to make quicker extra accurate debt choices based upon an increased set of offered information. AI-assisted underwriting supplies a 360-degree view of an applicant. It compiles big and also traditional information; social, business and also web information; and disorganized data. AI is playing vital function in scams avoidance by assisting to analyse customer behavior to anticipate or identify deceptive purchases. Making use of a equipment learning-based fraudulence discovery service could be trained to detect fraud within more than one sort of deal or application, or both of these at the very same time. Much of the talk about AI in banking has had to do with how innovation can change some features currently performed by humans. AI could also aid financial organisations offer their customers much more properly by offering them less complicated access to pertinent information. It is thought around 50% of hand-operated work might be automated. These roles normally consist of physical activities in very predictable and organized environments, as well as information collection and also information handling. Refine automation is extremely useful for economic solution clients as their account applications, including lending and also saving, can be accelerated dramatically. According to Goldman Sachs, artificial intelligence as well as AI will enable ₤ 26 billion to ₤ 33 billion in yearly " price financial savings as well as new revenue possibilities" within the monetary industry by 2025. Obstacles to fostering of AI in economic services Many firms and fields delay in AI adoption. Establishing an AI strategy with clearly defined benefits, discovering talent with the ideal ability, getting over functional silos that constrict end-to-end release, and lacking ownership and also dedication to AI for leaders are among the barriers to fostering frequently mentioned by executives. Doing not have a culture of innovation-- stakeholders within organisations hold enormous power in the success of AI projects. Lots of economic organisations have tiny risk cravings this is infiltrated magnate on the ground in charge of IT improvement activities. When it concerns skill, training as well as upskilling are vital. But this shouldn't be just concentrated on the modern technology groups. Company teams additionally require to be upskilled in the art of the possible when it comes to AI, in addition to some of the drawbacks and other factors to consider. Information infrastructure - monetary services firms typically experience as their data is often siloed throughout multiple innovations and teams, with analytical capabilities commonly focused on particular use situations. The requirement to standardise information as well as guarantee information is accessible is essential. Data privacy as well as cyber safety - making use of personal details are vital problems to attend to if AI is to know its potential. The General Information Security Guideline (GDPR), which introduced more stringent authorization requirements for information collection, provides individuals the right to be neglected and also the right to object which is a positive step in the right direction. Cybersecurity and also scams that could adjust commit large fraudulence are likewise a worry. Scrutinised expenses - Expenses in AI tasks are usually scrutinised by money and senior leaders as the initial ROI is low. AI capabilities are lasting critical investments so higher returns would be anticipated further down the line. Verdict AI provides technical chances like nothing else. Unleashed from the orbit of sci-fi, this is a real-world technology that prepares to be executed in any kind of business-- today. The capabilities of AI modern technologies will certainly remain to expand tremendously as large data collections required for training AI options end up being extra easily accessible. The time to move on AI is currently. Low obstacles to entry will bring ever before fiercer competitors for AI skill, AI licenses and also AI capacities. AI embraced early will transform the method financial institutions arrange, run, speed up and also achieve growth. By executing new cutting-edge modern technologies, economic organisations will endeavour to reduce prices and also create far better experiences for customers and also workers alike. This calls for organisations to totally reassess their total business procedures including their labor force, a cultural change is needed to welcome brand-new ways of working and also modern technologies.

The usages and also abilities of AI remain to expand and alter on a daily basis. This short article highlights necessary elements and benefits to be taken into consideration and additional expedition is urged. AI needs to not be considered a organization device or expansion of innovation however rather as a transformative cultural change that needs to be considered in a very wide, multi-dimensional context. Introducing Sandstone's Digital Intelligent Confirmation Assistant | QUEEN Sandstone's Digital Intelligent Confirmation Assistant (DiVA) makes the most of the power of AI to automate your source analysis, all while supporting regulative compliance. Queen makes verification straightforward as well as fast, freeing up sources, decreasing human error and ensuring a frictionless and much more clear consumer experience. DiVA automates every little thing from indexing and translating info to identifying missing out on information, verifying information, editing and drawing out details and consumer lending regulations providing it in a logical circulation format for assessors. You can evaluate financial institution declarations, payslips and also purchase info conveniently, transforming them right into machine-readable data. Utilize your admin console to establish regulations that match your inner information and also plan rules. And you can deploy as well as examine new features rapidly as well as safely as we present them into the system as part of our continuous r & d program. For those that wish to develop a small offshore account under reporting limitations, or merely to have the bank account developed because future organization, Hong Kong is additionally eye-catching offered the low minimum deposits required by the major financial institutions there. The minimum checking account equilibrium can be as reduced as HK$ 3,000. Naturally, you can't expect red carpet, VIP exclusive banking at this degree - yet you obtain a completely great working savings account with all the technological trimmings. Offshore Corporate Bank Accounts in Hong Kong - Do's and also Do n'ts. Generally, offshore clients select to charge account utilizing corporations, rather than personal accounts. This not just uses greater privacy, yet also flexibility and also can - depending naturally on just how things are structured - offer substantial tax obligation and also possession protection benefits. Accounts can easily be opened both for pure offshore companies like Panama, BVI, Nevis or Marshall Islands, or for regional Hong Kong firms that are established using candidate supervisors as well as investors.

When contacting local corporate provider in Hong Kong, you'll discover that a lot of these corporate service providers will certainly recommend you utilize a Hong Kong business to open up the account. The factor they do this is that it's simpler and more successful for them. They can integrate a regional firm at inexpensive, opening up the bank account is smoother and also quicker with a regional firm, and they can carry on payment candidate director fees annually. However it might not be the appropriate thing for you. Whilst it is true that Hong Kong companies do not need to pay any tax supplied they do not make any kind of local resource earnings, carrying out such a firm is not so straightforward. As an example, Hong Kong business are required to file audited accounts annually. They have to submit web pages and pages of files to convince the Inland Earnings Department (HKIRD) that they do not have any kind of regional company, as well as, from practical experience, the HKIRD is getting much stickier concerning this. Long-established firms are usually left unmolested but freshly developed firms can anticipate a great deal of conformity work in their first couple of years. Again, this fits the Hong Kong corporate company that charge handsomely for such services. Another variable to consider is Controlled Foreign Corporation (CFC) regulations in your home nation. (For an explanation see Wikipedia) Numerous customers choose to establish LLCs as they can be dealt with as passthrough entities, vastly simplifying reporting requirements in some nations like the United States. Hong Kong corporations are not LLCs and also can not be treated as passthroughs for tax functions. My recommendations - thinking you do not mean to do any type of business in Hong Kong besides banking and also perhaps the occasional journey https://beterhbo.ning.com/profiles/blogs/9-things-your-parents-taught-you-about-10-min-loan to visit your cash - would certainly be to open the account for a business from a international offshore tax obligation place. It's a little bit even more work and also expense at the start, and the financial institution could ask you much more concerns, however it will certainly save you a great deal of money as well as migraines in the long term. If you want a regional feel and look for your business, many virtual workplace solutions are available. For those who intend to develop a tiny offshore account under reporting restrictions, or just to have the checking account established in view of future company, Hong Kong is also attractive provided the reduced minimum deposits required by the significant financial institutions there. The minimal checking account equilibrium can be as reduced as HK$ 3,000. Of course, you can not expect red carpet, VIP personal financial at this level - however you obtain a perfectly great working checking account with all the technological trimmings. Offshore Corporate Bank Accounts in Hong Kong - Do's and Do n'ts. Usually, overseas customers choose to charge account using companies, rather than personal accounts. This not just uses greater privacy, however also versatility as well as can - depending certainly on exactly how things are structured - offer significant tax and property security benefits.

Accounts can easily be opened both for pure offshore business like Panama, BVI, Nevis or Marshall Islands, or for regional Hong Kong companies that are established making use of candidate supervisors and also shareholders. When getting in touch with neighborhood business provider in Hong Kong, you'll locate that the majority of these company provider will certainly recommend you utilize a Hong Kong firm to open up the account. The factor they do this is that it's simpler and also a lot more successful for them. They can integrate a regional firm at inexpensive, opening the savings account is smoother as well as faster with a neighborhood firm, as well as they can carry on payment nominee supervisor charges each year. However it may not be the right thing for you. Whilst it is true that Hong Kong firms do not have to pay any type of tax obligation given they do not make any kind of regional resource revenue, carrying out such a business is not so easy. As an example, Hong Kong business are needed to file audited accounts yearly. They have to submit web pages and also web pages of documents to encourage the Inland Earnings Department (HKIRD) that they don't have any regional company, and also, from functional experience, the HKIRD is obtaining much stickier concerning this. Long-standing companies are usually left unmolested yet recently established companies can expect a lot of conformity operate in their initial couple of years. Once again, this suits the Hong Kong corporate provider that bill handsomely for such services. Another factor to consider is Controlled Foreign Company (CFC) regulation in your home nation. (For an explanation see Wikipedia) https://www.sandstone.com.au/en-gb/ Many clients choose to set up LLCs as they can be dealt with as passthrough entities, vastly streamlining reporting needs in some nations like the U.S.A.. Hong Kong companies are not LLCs and also can not be dealt with as passthroughs for tax obligation functions. My advice - assuming you don't mean to do any kind of business in Hong Kong besides financial and also probably the occasional trip to see your cash - would certainly be to open the account for a business from a international offshore tax obligation place. It's a little bit more job as well as expenditure at the start, as well as the bank might ask you a lot more inquiries, however it will certainly save you a great deal of money and also migraines in the long-term. If you desire a local look and feel for your business, many online office solutions are readily available. In 1997 the British returned sovereignty over Hong Kong to China. The former colony became one of China's two Special Management Areas (SARs), the other being Macau. Many people were initially uncertain concerning among the world's capitalist strongholds being run by a communist power, and at the time a great deal of investors took out, lots of taking their dynamic business acumen heading to areas like Singapore and also Vancouver. However, the "one country, two systems" design adopted by Beijing to accompany free market reforms and the growth of China into an financial superpower has actually confirmed very successful. The Basic Legislation of Hong Kong, the matching of the constitution, specifies that the SAR preserves a "high level of freedom" in all matters except international connections and defence. The SAR today runs as a significant overseas finance facility, discreetly oiling the wheels of commerce between East and West. These days, rather than being put off by the Chinese influence, many global financiers who are drawn in to Hong Kong are coming exactly as a result of this Chinese connection. Hong Kong is the point of access to Chinese trade, without the legal as well as cultural problems of doing business in landmass China. Those that do not trust their own governments are assured by the truth that under the Basic Law, Hong Kong's international relationships are run from Beijing. While most offshore territories humbly submit to demands from the United States and various other western nations, in the case of China, the connection is certainly turned around. Hong Kong does have a variety of Tax Information Exchange Agreements (see listed below) but these are sensibly policed as well as do not enable fishing expeditions. Offshore Banking in Hong Kong The area's populace is 95 percent ethnic Chinese and also 5 percent from other groups, however English is really widely talked as well as is the main language in businesses like financial. One thing I like concerning making use of Hong Kong for overseas savings account is the same disagreement I have used for Panama and Singapore: it's a ' actual' country with actual profession going on. The Find more info Hong Kong dollar is the 9th most traded currency on the planet. Contrast this to doing business on a tiny island or various other remote banking jurisdiction, where everybody understands your only factor for doing business there is offshore banking. It also means that there is not a problem doing your banking in cash, if you so wish. In the meantime the HKD, the local dollar, still tracks extremely closely the United States buck, yet this seems changing as the Chinese Yuan distributes freely in Hong Kong, both in money as well as in financial institution deposits. We believe this stands for an superb chance to expand funds out of the United States buck now, gaining exposure to Chinese growth in the meantime. ( Naturally, you can additionally hold HKD in financial institutions in other parts of the globe as well). Bank accounts in Hong Kong are mostly all multi-currency by default, permitting all significant local and also international currencies to be held under one account number as well as exchanged openly and also instantaneously within the account at the click of a mouse.

There is no resources gains tax obligation, no tax on bank rate of interest or stock exchange financial investments, and no tax on offshore sourced income. This, combined with a inviting mindset to non-resident customers in the banks ( consisting of US people incidentally, that are usually unwanted in traditional offshore banking places like Switzerland), and strong cultural and lawful regard for economic privacy, makes Hong Kong among Asia's finest overseas financial jurisdictions. In 1997 the British returned sovereignty over Hong Kong to China. The previous nest turned into one of China's two Unique Management Regions (SARs), the various other being Macau. Lots of people were at first doubtful concerning among the globe's capitalist bastions being run by a communist power, and also at the time a lot of financiers took out, many taking their vibrant business acumen heading to locations like Singapore and Vancouver. Nonetheless, the "one nation, two systems" version taken on by Beijing to accompany free enterprise reforms and the growth of China into an economic superpower has proven very successful. The Basic Regulation of Hong Kong, the equivalent of the constitution, stipulates that the SAR preserves a "high level of freedom" in all issues except foreign relationships as well as defence. The SAR today runs as a significant overseas money center, quietly fueling oil the wheels of commerce between East and West. Nowadays, instead of resenting the Chinese influence, the majority of global capitalists who are drawn in to Hong Kong http://www.bbc.co.uk/search?q=online banking are coming specifically as a result of this Chinese link. Hong Kong is the point of access to Chinese trade, without the lawful and also cultural troubles of doing business in landmass China. Those that do not trust their own federal governments are guaranteed by the reality that under the Basic Regulation, Hong Kong's international connections are run from Beijing. While a lot of offshore jurisdictions humbly submit to demands from the United States as well as various other western nations, when it comes to China, the partnership is most definitely turned around. Hong Kong does have a variety of Tax obligation Information Exchange Agreements (see listed below) however these are smartly policed as well as do not permit fishing expeditions. Offshore Banking in Hong Kong The area's populace is 95 percent ethnic Chinese as well as 5 percent from other teams, yet English is extremely extensively talked and is the major language in businesses like banking. One thing I such as concerning utilizing Hong Kong for offshore checking account is the same debate I have used for Panama and also Singapore: it's a 'real' nation with real profession taking place. The Hong Kong dollar is the ninth most traded currency in the world. Contrast this to doing organization on a little island or various other remote financial territory, where everybody recognizes your only factor for working there is overseas banking. It likewise suggests that there is not a problem doing your banking in money, if you so desire. In the meantime the HKD, the neighborhood buck, still tracks really carefully the US buck, yet this seems transforming as the Chinese Yuan flows openly in Hong Kong, both in money and also https://www.sandstone.com.au/en-gb/ in financial institution deposits. We think this represents an superb possibility to diversify funds out of the US buck now, getting direct exposure to Chinese growth in the meantime. ( Certainly, you can likewise hold HKD in financial institutions in various other parts of the world as well). Checking account in Hong Kong are almost all multi-currency by default, allowing all major regional and international money to be held under one account number and traded freely and instantly within the account at the click of a mouse.

There is no funding gains tax, no tax obligation on financial institution interest or securities market financial investments, as well as no tax obligation on offshore sourced revenue. This, integrated with a inviting attitude to non-resident customers in the banks (including US residents by the way, that are usually unwanted in typical overseas banking places like Switzerland), and also solid cultural as well as lawful regard for economic personal privacy, makes Hong Kong one of Asia's ideal overseas financial territories. All financial institutions as well as banks have a Digital Financial platform these days. However does yours simply cover the essentials? Or have you knew the fast-growing importance of this network for your clients as well as your financial institution's future? Progressively, it's the network your existing clients pick to connect with you in. And as the electronic indigenous generation reaches adulthood and also the workforce, it will certainly be the only network they'll use-- to study, use as well as utilize their banking products and services. It's time to get serious regarding Digital Financial Your financial institution's future depends upon the value you position on Digital Banking. Exactly how you prioritise its financial investment and also how dedicated your teams are to including Digital Banking right into their critical choices. Without a durable Digital Financial platform that can grow with you, react to adjustments as well as possibilities easily and supply extraordinary service to your clients, you're at danger of falling behind your competitors. Include Open Banking to the equation When Open Banking starts its staged execution from July 2019, your consumers will have the power to transform financial institutions and their services-- with the click of a computer mouse or a faucet on their smart phone. The obstacles to relocating financial institutions will certainly be gone. So, what will make consumers remain with you? Your rates? Brand name loyalty? You require to act now to ensure your consumers select to remain. As well as those banks who pick to concentrate on their Digital Banking platform are making the appropriate choice. Excellent assumptions Clients have excellent expectations of their Digital Banking system. These expectations go means beyond just examining a checklist of their deals or transferring funds. It stands to reason you're going all out to satisfy their expectations, right? No? Opportunities are your inner group is all out as it is, just to guarantee you're compliant with regulations. They do not have consumer lending time to scratch themselves, not to mention move past the absolute essentials. So you had an skilled partner on board. A partner that could: guarantee you were compliant

quickly incorporate with your core banking system assimilation springboard you right into a Digital Banking future so you can constantly supply an exceptional consumer experience The important active ingredient Is Digital Banking on the schedule at most of your bank's inner conferences? It's not? It should be. Ideally it must be one of the initial items on every schedule, because it's the essential ingredient to your bank's future. As we have actually noted, your Digital Financial system is increasingly the only place customers engage with your bank. Soon, it'll be the only way you can connect, cross-sell as well as upsell to them. And the only means you can add worth to their experience with education and learning as well as tools to encourage their monetary administration. Future-proof your Digital Financial approach It's vital that you purchase a future-proof Digital Financial technique. One that is concentrated on increasing and also maintaining uptake of your Digital Financial system. And also you need to obtain the entire organisation on board. Your Digital Financial approach must be driven from the top down as well as penetrate with every decision in the organisation. It needs to remain in your bank's DNA. Open Up Banking Opportunities You understand Open up Banking is right here. Yet apart from making certain that you're certified with all the laws, have you taken into consideration the opportunities it uses? It's time to take a look at exactly how you can harness the sharing of details that will certainly include Open Financial. For example, at a client's request, you could be positive and also offer them custom bargains, based upon an analysis of their information. To do this, you require: an reliable application programming user interface (API) to make it possible for protected and robust data sharing. the strong structure of an functional Digital Financial platform that is adaptable sufficient to expand with you. as well as above all, an seasoned partner. A partner that knows the market from top to bottom. Someone who can identify brand-new opportunities, as well as aid you make them happen-- from a solid base. Without this a person, you can obtain left method behind in the rush for the chance market share by well-prepared organisations as well as new economic kids on the block. |

Archives

March 2023

Categories |

RSS Feed

RSS Feed